Recent high and volatile electricity prices, driven in part by movements in wholesale gas prices, have kept energy markets in the public eye.

While policymaker attention was initially directed towards ways of addressing the impacts on energy consumers in the short-run, focus has now shifted to how wholesale power market arrangements work and whether they could be reformed over the medium- to long-run to deliver the best outcomes for consumers.

How best to achieve these objectives and address the necessary trade-offs between them is currently the subject of discussion in the EU (following the Commission’s March 2023 Electricity Market Design proposal), many EU member states and the UK (the Review of Electricity Market Arrangements process). Some of the potential changes being discussed could (and indeed are partly intended to) have important impacts on investment signals in the power sector, which will need to undergo a profound transformation in the coming decades as it decarbonises.

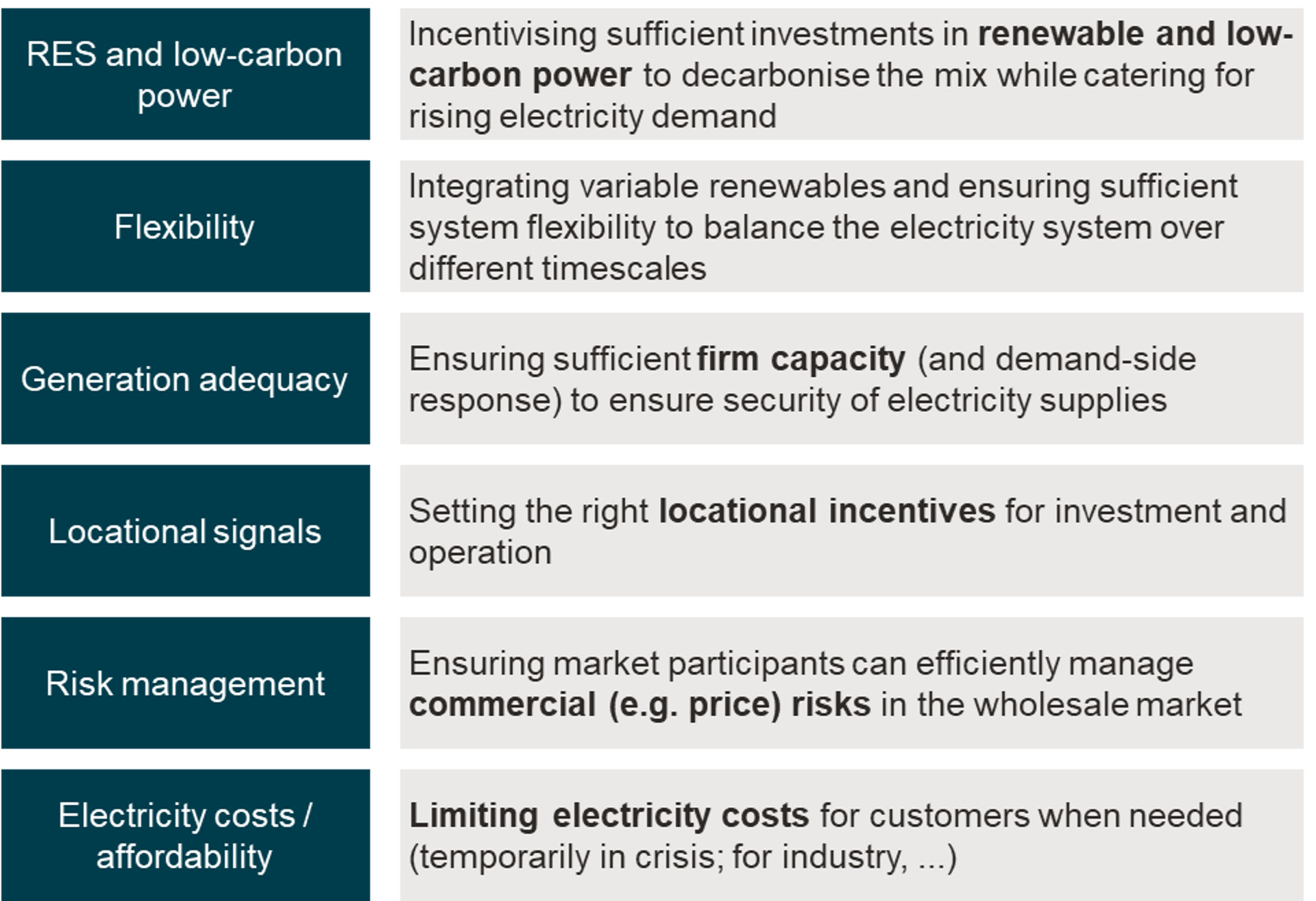

Over the coming months, Frontier experts will be discussing the impacts of potential reforms, and the extent to which they are likely to help achieve decarbonisation of the power sector at least cost over the longer-term with stakeholders in the industry. We will initially be focussing on issues related to low-carbon and renewable power, flexibility and locational signals. This article provides a brief overview of the issues and some of the key questions policymakers will need to address.

Background: Rising electricity demand and the need for mass low-carbon power

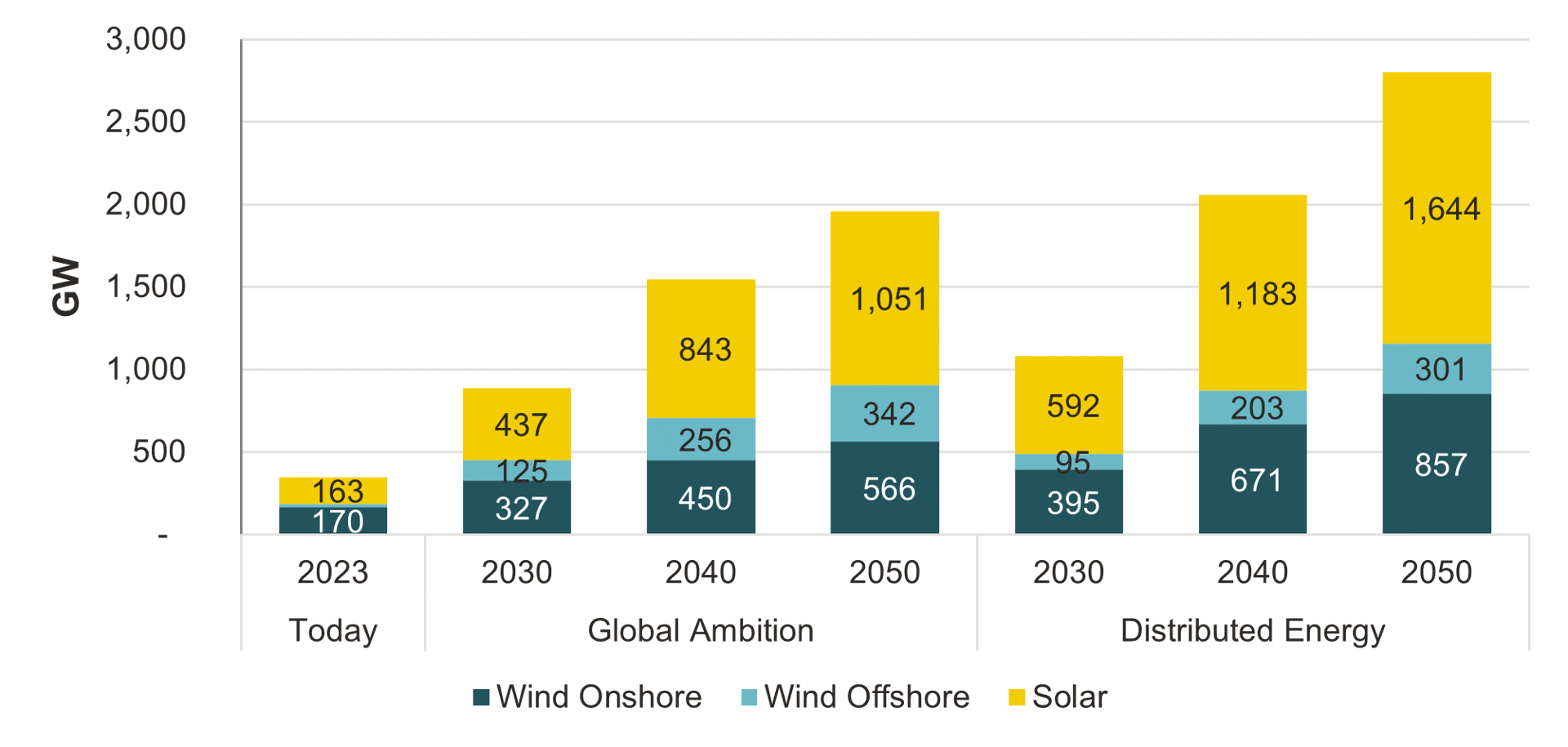

Decarbonisation of the European energy system is likely to involve a massive increase in power demand. While there is some uncertainty as to the precise extent of any increase, some scenarios show around a doubling in the amount of electricity consumed annually, as the heating, cooling, industry and transport sectors increasingly electrify. Furthermore, electricity will be used in new applications such as the production of low-carbon hydrogen and e-Fuels. Coupled with the phase out of existing generation (mainly coal-fired plants and, in some cases, nuclear), the transition required will be profound.

Clearly, the cornerstone of the transition will be mass low-carbon power. While some countries may invest in new nuclear power or fossil generation combined with carbon capture and storage, the vast majority of new capacity growth will come from renewable capacity – the production of which is largely weather-dependent. Build rates will need to increase substantially if Net Zero goals are to be met.

Figure 1: Wind and PV capacities for EU-27 according to TYNDP 2022 Global Ambition and Distributed Energy scenarios

Source: TYNDP 2022, RES capacities under scenarios Global Ambition and Distributed Energy. Today’s values were taken from ENTSO-E Transparency Platform in “Installed Capacity per Production Type” data page

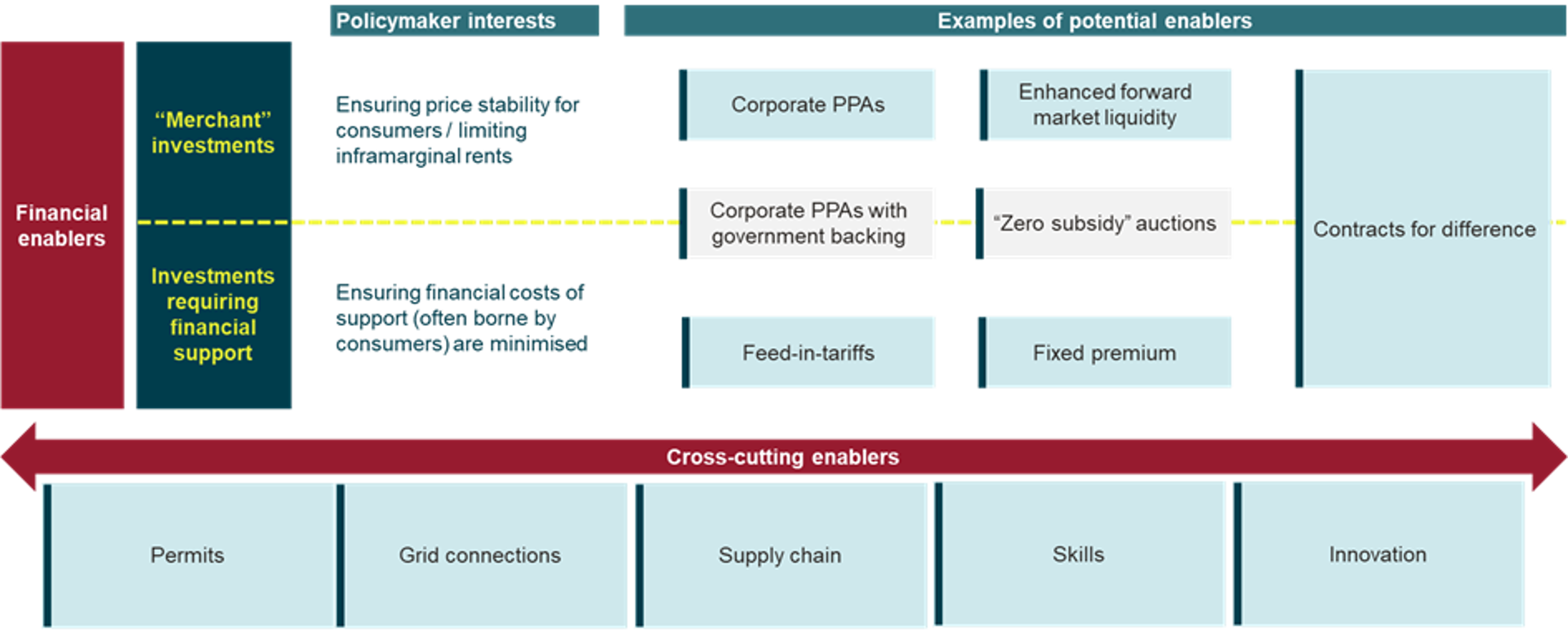

Unlocking the required investment in carbon neutral power generation capacity will require addressing critical issues in relation to planning and grid connection processes as well as the supply chain. But while these are necessary pre-conditions, they are not sufficient. Investors also require sustainable business models.

There have been some favourable tailwinds. Costs for solar and wind have come down significantly in recent years. And carbon prices are now substantially higher than 2-3 years ago.

However, the business case for investment in intermittent renewables is undermined in part by the transition itself. As more capacity is deployed, there will be increasingly frequent periods of excess supply of low marginal-cost low-carbon generation, leading in turn to more periods of low/zero prices. And the interventions to claw-back “windfall profits” from existing plants during the crisis may have exacerbated perceptions of policy-related risks faced by investors.

Flexibility and adequacy

In the early 2010s, countries across Europe considered how best to ensure sufficient “firm” capacity to ensure security of electricity supplies, and whether additional incentives, beyond the signals provided by an “energy only” market, were required. The EU has settled for an approach whereby each Member State can choose whether or not to introduce so-called “capacity mechanisms” and, if so, what type (albeit subject to certain conditions).

However, capacity mechanism designs are likely to need to evolve as the electricity sector transitions towards Net Zero, to better accommodate sources such as RES, demand-side response, and new forms of storage.

In addition, in many markets, the emphasis will increasingly be on flexibility across different timescales (rather than “firmness”), to ensure the system remains balanced given variations in intermittent generation. Both the UK and the EU reform processes are considering the possibility of dedicated flexibility mechanisms or reforms to existing capacity mechanisms to enhance longer-term investment signals for flexible capacity. But the discussion on exactly how such schemes should be designed (in particular, the nature of the flexibility “product” that would be purchased) is as yet immature. Furthermore, the roles of operators of the transmission and distribution grids are evolving continuously, with the need to adjust and re-calibrate responsibilities, systems and processes.

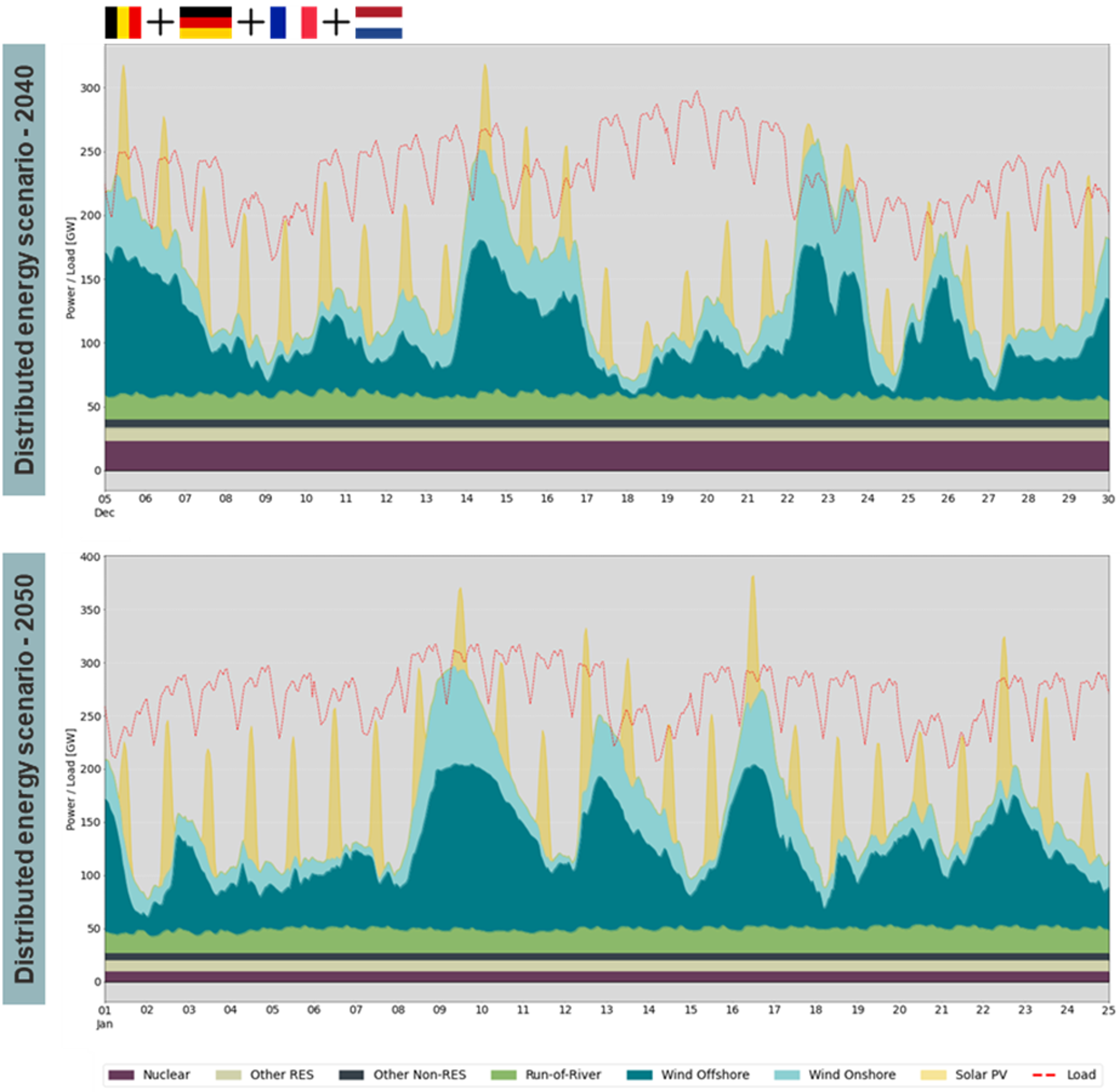

Figure 2: Electricity generation and demand during a dunkelflaute period – examples from Western Europe for 2040 and 2050

Source: Frontier Economics based on TYNDP 2022 data

Note: Production profiles for RES for the first figure are based on Dec 1995 while for the second are based on Jan 2010 which has been similarly stressful in terms of weather conditions as 1995 according to TYND 2022

Location

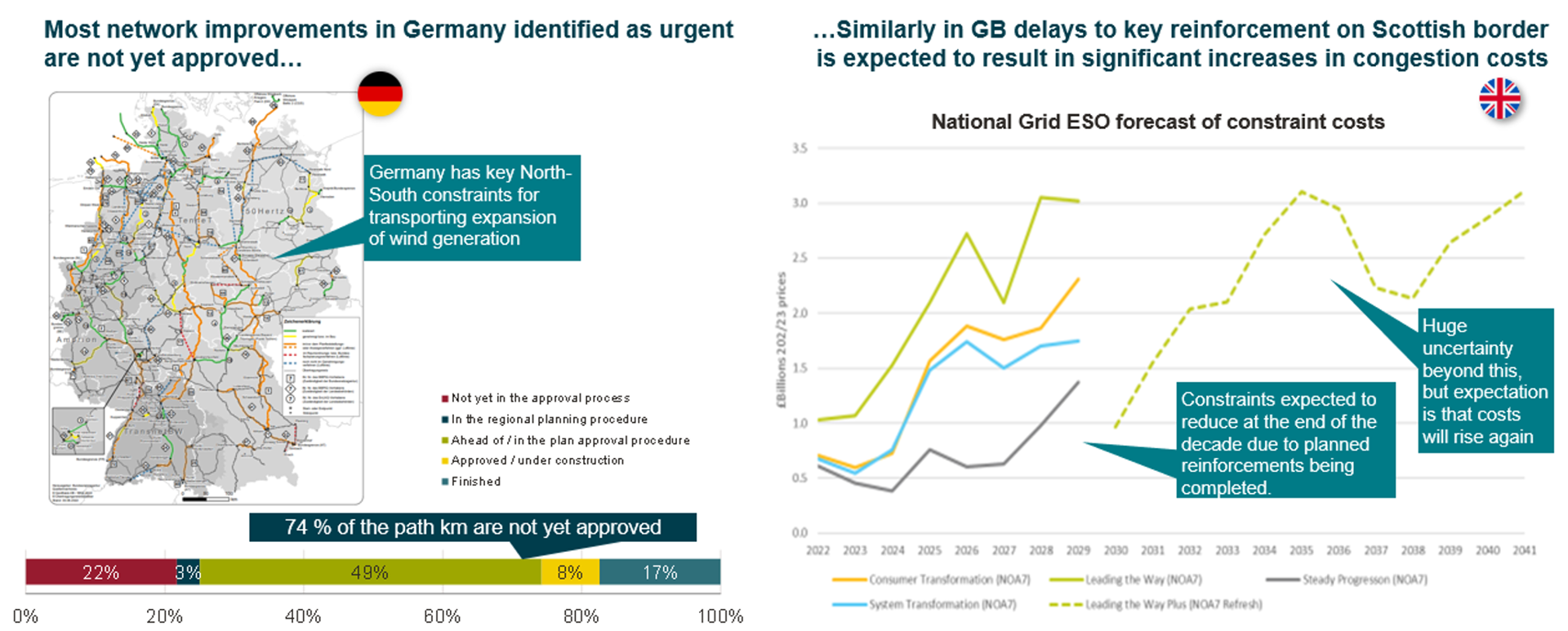

In addition, the lowest-cost renewable potential is not necessarily located close to existing demand centres or existing grid capacity. Ensuring new low-carbon power can flow to where it is needed will therefore require substantial new grid connections and reinforcements to existing lines. But there are limits on the extent and speed of upgrades to the grid – policymakers will also need to consider how best to make efficient use of available network capacity, respecting the constraints in the grid.

Sources: Germany – BNetzA (2022): Monitoring des Stromnetzausbaus Zweites Quartal 2022; UK – National Grid ESO forecast

To address this, the UK is weighing up a move to “locational marginal pricing” – whereby wholesale prices would be set to reflect supply and demand at each “node” in the grid (as opposed to the current system of a single price for whole of Great Britain, with constraints separately managed by the system operator). The EU similarly has an ongoing process (albeit separate to the Electricity Market Design proposal discussions), reviewing existing “bidding zones” and (broadly) whether some should be split. However, much of the analysis carried out to justify such moves relies on overly simplistic assumptions, and important evidence gaps remain regarding the overall impacts.

The need for a holistic view

The added challenge is that it is difficult to think about reform in any one of these areas in isolation. For example, support mechanisms could be designed to give generators greater exposure to wholesale market signals. But whether this leads to more efficient investment choices will depend on whether wholesale market signals already reflect the full range of system impacts that technologies might have. Similarly, the precise implications of any move to more granular locational wholesale pricing will depend crucially on existing approaches to network charging, congestion management and the design of any support mechanisms, including whether the latter include any locational signals. (It is notable that the review process in the UK is arguably more far-reaching than the EU process, covering all aspects of market design.)

The interest in longer-term contracting for renewables, firm capacity and flexibility suggests that policymaker decisions (rather than those of the market) will drive the mix of technologies on the system for a while yet. However, it is not clear from the debate that policymakers have explicitly recognised this or explicitly assessed whether the benefit of correcting possible market failures outweighs the risk of policy failure from greater interventionism.

Key questions for the current discussion

These trade-offs are also important when considering questions relevant to the current debate. In our webinar discussions, we will be focussing initially on three of the aspects, and provide some indication of the ground we hope to cover:

- Low-carbon support:

- How will mechanisms such as Contrats for Difference (CfDs) affect the costs of the energy transition, and how do the impacts depend on both strategic energy policy choices as well as specific CfD design choices?

- How can low-carbon capacity manage their risks in the market? What are the impacts of CfDs on the internal electricity market?

- What should be the relative role of Power Purchase Agreements (PPAs) vs. CfDs in the market? What role should policymakers have in shaping the market for PPAs?

- Flexibility:

- What business models are required to support investments in flexibility (at both transmission and distribution level) and adequacy, while ensuring that capacity responds efficiently to wholesale market signals? What future market designs could provide an efficient amount and the right types of flexibility?

- What roles should operators of the transmission and distribution grids have in a re-calibrated system?

- Locational signals:

- What high-level approaches are there for strengthening locational signals?

- What assumptions may underlie the case for and against a move to more granular locational price signals in the wholesale market? What are the alternatives?